The lines between traditional businesses and financial services are blurring. From ride-sharing apps offering loans to e-commerce platforms providing payment solutions, businesses across industries are embedding financial services directly into their offerings. This transformation, known as embedded finance, is redefining customer experiences and creating new revenue streams. But why is this happening, and what does it mean for businesses and consumers? Let’s explore the fintech revolution happening across industries.

Embedded finance refers to the seamless integration of financial services into non-financial platforms. Instead of relying on traditional banks, businesses can now offer financial products such as payments, lending, insurance, and investment solutions directly within their ecosystem.

Examples include:

Modern consumers demand seamless, integrated experiences. They no longer want to visit a bank for financial services—they expect businesses to provide them within their everyday interactions. This shift is driving companies to embed fintech solutions into their platforms.

Businesses that incorporate financial services can tap into new revenue streams by:

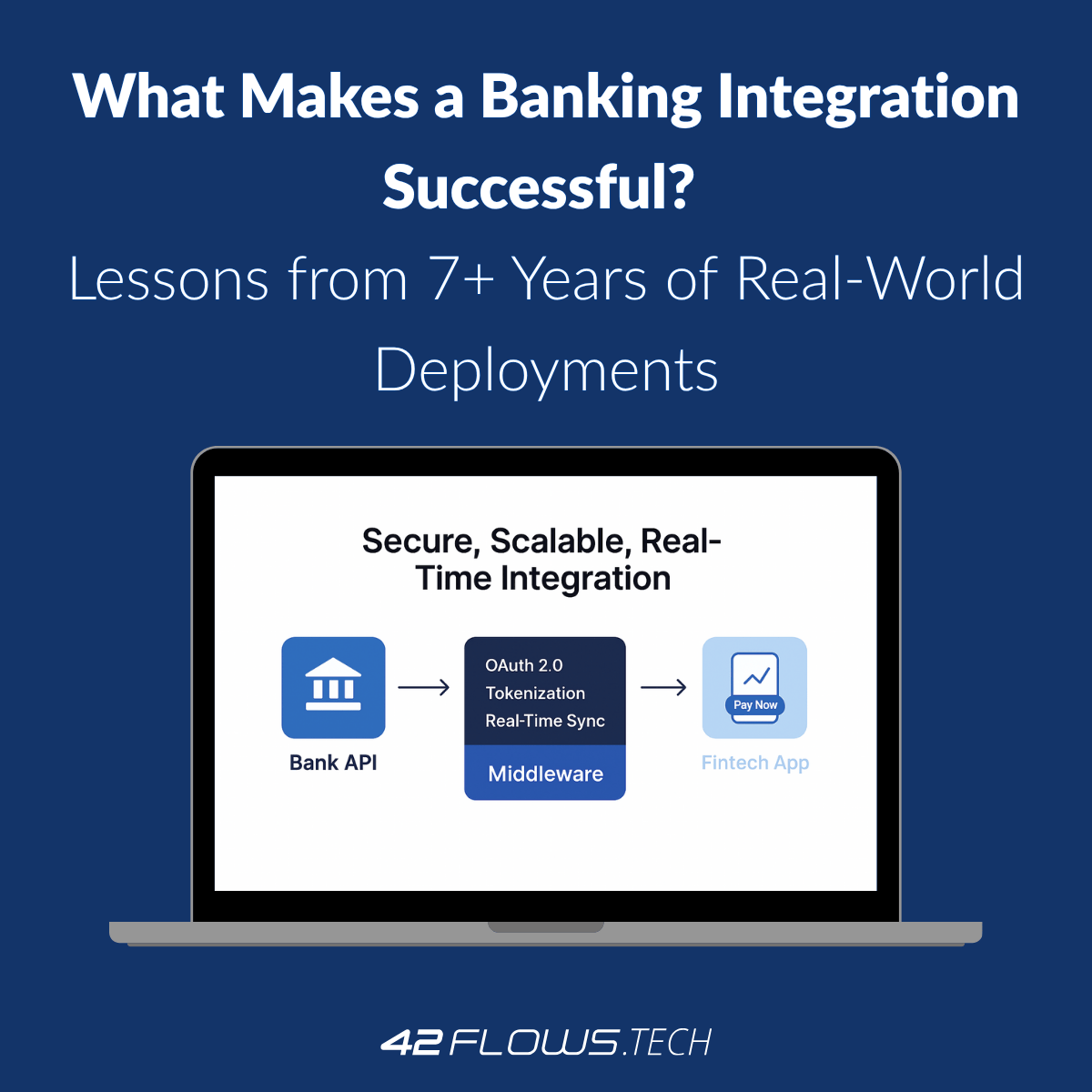

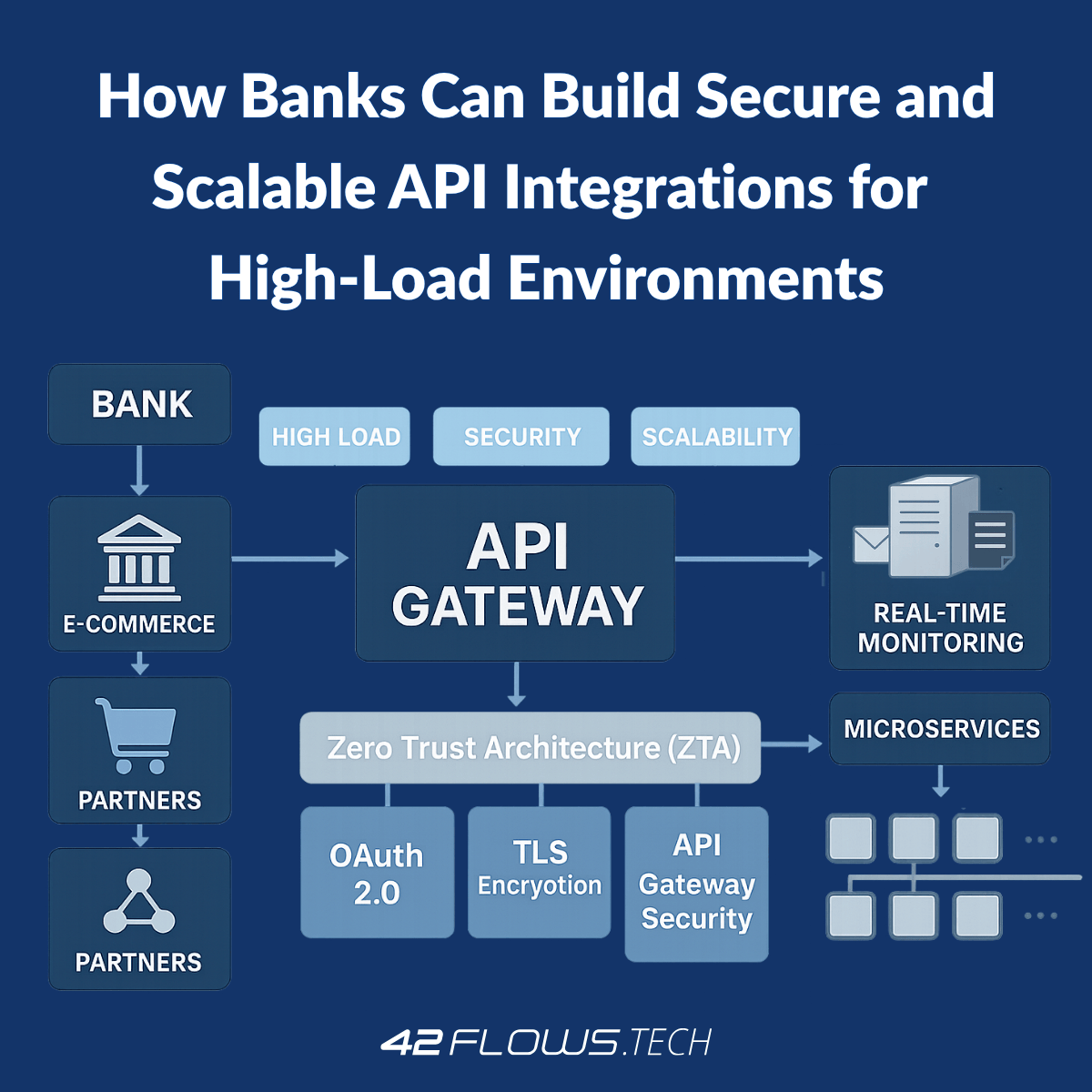

Open banking and API technology have made it easier than ever for non-financial businesses to integrate financial services. Instead of building banking infrastructure from scratch, companies can partner with fintech providers to offer services like:

When businesses offer embedded financial services, they create stickier customer relationships. For example:

Governments worldwide are encouraging financial innovation through open banking regulations (e.g., PSD2 in Europe). This has allowed more companies to access financial infrastructure and offer regulated services without being banks themselves.

While embedded finance presents exciting opportunities, businesses must address key challenges:

As technology advances, we can expect even deeper fintech integration across industries. Some future trends include:

Every business is becoming a fintech because customers demand convenience, and technology has made it easier than ever to integrate financial services. Companies that embrace embedded finance gain a competitive advantage, increase revenue, and enhance customer loyalty. As financial technology continues to evolve, the businesses that innovate today will lead the market tomorrow.

Want to explore embedded fintech solutions for your business?

Contact us today! Email us at success@42flows.tech, and we will help you implement an effective solution.

Let’s talk. Just enter your details and we will reply within 24 hours.

Maksym Popov

Maksym Popov