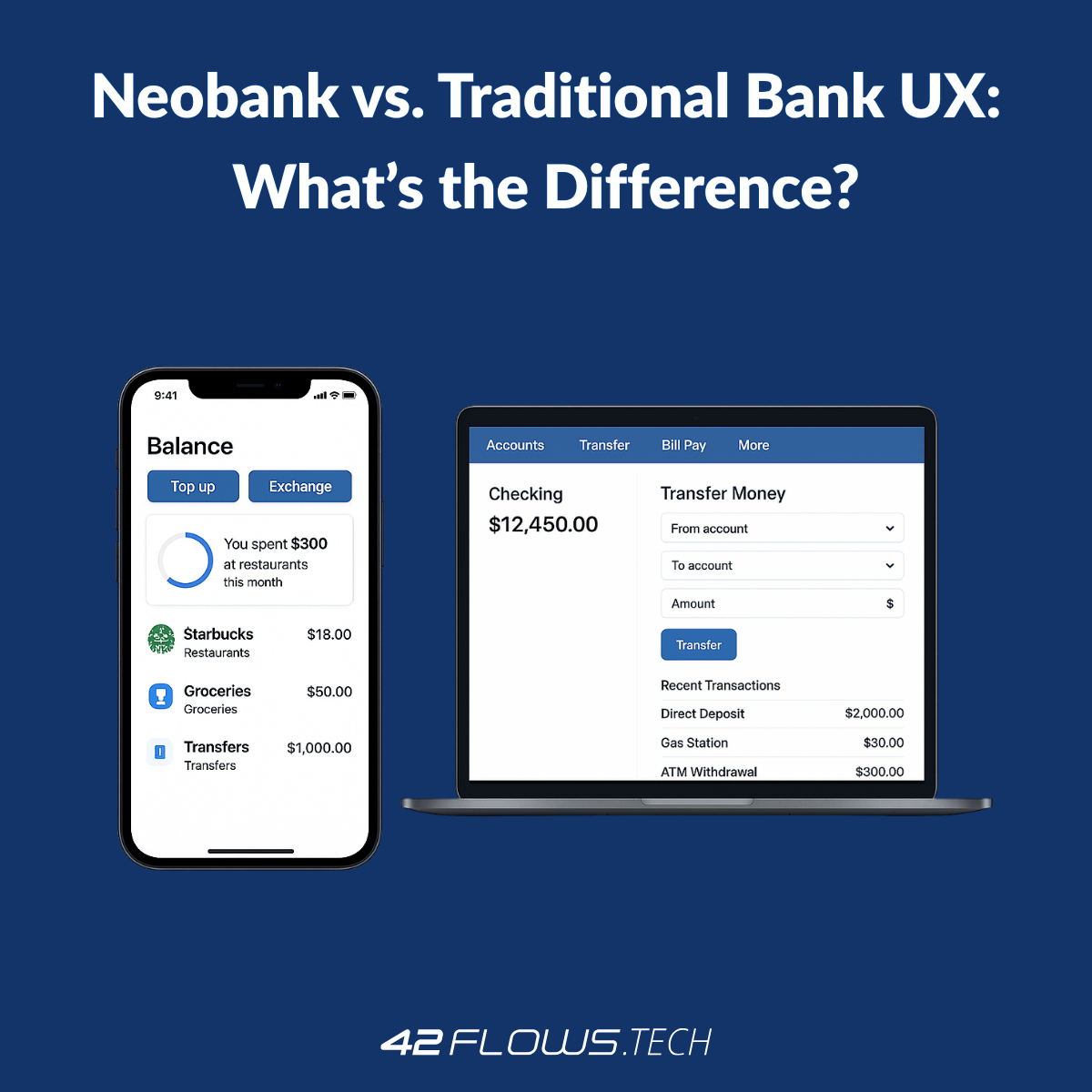

The banking industry has undergone a massive shift in recent years, with neobanks—digital-first, branchless banks—disrupting traditional financial institutions. While legacy banks still hold the majority of market share, neobanks are rapidly gaining ground, largely due to their superior user experience (UX).

Unlike traditional banks, which often modify existing infrastructure to fit digital channels, neobanks are built for digital-first experiences from the ground up. This difference in approach leads to vastly different UX strategies.

So, how do neobanks design seamless, frictionless banking experiences, and where do traditional banks still struggle? This article compares their UX approaches and explores how both types of institutions can optimize for the future.

Neobanks prioritize mobile-first, user-centric design with:

Since neobanks don’t have physical branches, their UX is optimized for self-service. Every interaction, from opening an account to disputing a transaction, is designed to be completed within the app without needing human intervention.

Most traditional banks were built for in-person banking first. While they now offer online and mobile banking, many still:

This “digital adaptation” approach often results in fragmented experiences, where customers must switch between online, mobile, and in-person interactions to complete a single process.

Example: Revolut and N26 allow users to open an account in under 10 minutes, compared to traditional banks that may take days or weeks.

Many customers abandon sign-ups midway due to unnecessary friction, which is why traditional banks are increasingly adopting hybrid digital onboarding solutions to streamline this process.

Neobanks often use gamification and micro-interactions to make banking more engaging and less intimidating.

Traditional banks need to focus on UX decluttering—simplifying menus, prioritizing essential features, and ensuring mobile-friendly designs.

Many legacy banks are improving by implementing real-time payments (RTP) and blockchain-based transaction processing, but they still have a long way to go to match neobank efficiency.

While AI-powered banking assistants are emerging in legacy institutions, traditional banks still lag behind in automated customer service efficiency.

Many traditional banks are catching up by adopting passwordless logins, biometric verification, and behavioral authentication, but the experience still varies widely.

Category |

Neobanks (Digital-First) |

Traditional Banks (Digital-Adapted) |

|---|---|---|

| Onboarding | Instant, paperless, AI-driven | Manual, often requires branch visits |

| Navigation & UI | Simple, mobile-first UX | Complex, sometimes cluttered |

| Transactions | Real-time payments, instant P2P | Often slower, delays in international transfers |

| Customer Support | AI-first, 24/7 chatbots | Call centers, slower response times |

| Security | Biometric-first, AI fraud detection | Secure but sometimes inconvenient |

| User Engagement | Gamification, personalized insights | Traditional, limited personalization |

✔ Faster, more intuitive onboarding

✔ Mobile-first experience with real-time updates

✔ AI-driven automation for efficiency

✔ Deeper financial product offerings

✔ Established trust and regulatory experience

✔ Larger physical network for in-person services

The future of banking UX lies in a hybrid approach. Traditional banks are investing in fintech collaborations and digital transformation, while neobanks are working on expanding their financial product range.

At 42Flows, we help financial institutions modernize their digital banking UX, streamline customer journeys, and integrate AI-driven banking experiences.

Let’s talk. Just enter your details and we will reply within 24 hours.

Maksym Popov

Maksym Popov